UMID or Unified Multi-Purpose ID is a government-issued ID that can be used for a variety of purposes. It can be used to verify your identity, apply for loans, open bank accounts, and acquire government services. Also, it is considered a primary valid ID.

It is an essential document for every Filipino citizen, as it provides access to various benefits and services offered by the SSS.

The best part is, it’s free for your first application!

How to Register for SSS UMID

1. You have the option to set an appointment or walk into your preferred SSS branch.

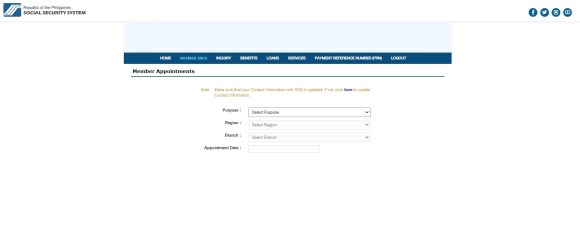

Online appointment system – You can set an appointment via your My.SSS at your preferred SSS branch. This option is best if your SSS branch doesn’t allow walk-ins.

Branch Walk-in – Following the mandatory SSS Number Coding Scheme for over-the-counter transactions.

2. Prepare your requirements for UMID:

UMID application form

1 Primary valid ID

List of Primary valid ID

Passport

Driver’s License

SSS Card

PRC ID

Seaman’s Book

Voter’s ID

3. Visit the SSS branch where you have a set appointment with your supporting documents both original and photocopy.

4. Have your photo and biometrics taken. Double-check your information before they finalize it.

5. Your UMID Card will be processed. It usually about 30 working days to receive a UMID Card application.

6. Pick up your UMID Card. You will be informed via SMS or email when it is ready for pick-up.

It’s now easy to schedule an appointment for the Social Security System (SSS) has been made incredibly easy and convenient. With the advancement of technology, the SSS has implemented an online appointment system, allowing individuals to book appointments from the comfort of their homes.

You can select your preferred date, time, and location for their appointment. The system provides a user-friendly interface that guides applicants through the process step by step, ensuring a seamless experience. This online scheduling system has significantly reduced the need for long queues and waiting times at SSS branches, providing applicants with a more efficient and hassle-free way to secure an appointment for their UMID card.

Imagine being accepted into your dream school—the prestigious institution that aligns perfectly with your aspirations, values, and educational goals. The prospect of walking through its hallowed halls, engaging in thought-provoking discussions with brilliant professors, and joining a vibrant community of like-minded individuals is undeniably enticing. Yet, the reality of tuition fees, accommodation expenses, and other educational costs often becomes a roadblock on this path.

For many students, the dream of attending their ideal college or university can seem like an unattainable aspiration, hindered by the overwhelming financial burden.

Fortunately, corporate scholarships have emerged as a powerful resource, bridging the gap between talent and accessibility. These scholarships, offered by esteemed corporations across various industries, not only provide financial assistance but also pave the way for mentorship, career opportunities, and professional growth.

List of Corporate Scholarships for Filipino Students

PLDT-Smart Foundation Scholarship Program

The PLDT-Smart Foundation Scholarship Program offers opportunities for financially challenged but academically gifted students to pursue their college education.

The scholarship covers tuition fees, monthly stipends, and book allowances. Scholars are selected based on academic performance, leadership potential, and socioeconomic status.

Coca-Cola Foundation Philippines Scholarship Program

The Coca-Cola Foundation Philippines Scholarship Program aims to provide financial assistance to talented and deserving students from low-income families.

The scholarship covers tuition fees, allowances, and other educational expenses. Applicants are evaluated based on academic excellence, leadership potential, and community involvement.

San Miguel Foundation Scholarship Program

The San Miguel Foundation Scholarship Program aims to empower economically disadvantaged students by providing them access to quality education.

The scholarship covers tuition fees, book allowances, monthly stipends, and other academic expenses. Scholars are selected based on their academic performance and financial need.

BDO Foundation Scholarship Program

The BDO Foundation Scholarship Program assists deserving students who lack the financial means to pursue a college education.

The scholarship covers tuition fees, allowances, and book grants. The program focuses on students from low-income families who have achieved excellent academic records.

Jollibee Foundation Scholarship Program

The Jollibee Foundation Scholarship Program aims to support financially disadvantaged but academically talented high school graduates who wish to pursue a college education.

The program covers tuition fees, monthly allowances, and book allowances for selected scholars.

SM Foundation Scholarship Program

The SM Foundation Scholarship Program is designed to assist underprivileged but deserving students in their pursuit of higher education.

The program offers full scholarships, including tuition fees, monthly allowances, and other academic expenses. Scholars are selected based on their academic performance, leadership potential, and socioeconomic status.

Aboitiz Foundation Scholarship Program

The Aboitiz Foundation Scholarship Program supports exceptional students from underprivileged backgrounds who wish to pursue higher education.

The scholarship covers tuition fees, allowances, and other educational expenses. Applicants are evaluated based on academic excellence, leadership potential, and socio-economic status.

Ayala Foundation Scholarship Program

The Ayala Foundation Scholarship Program provides financial assistance to outstanding students who come from economically disadvantaged backgrounds.

The scholarship covers tuition and other school-related expenses. Ayala Foundation also offers specialized scholarships for engineering and business courses.

Metrobank Foundation Scholarship Program

The Metrobank Foundation Scholarship Program aims to develop a pool of future leaders in various fields. It offers financial assistance to deserving students who demonstrate exceptional academic performance, leadership potential, and a commitment to community service. The scholarship covers tuition fees, monthly stipends, and other allowances.

Globe Telecom Scholarship Program

Globe Telecom’s scholarship program provides educational opportunities for talented Filipino students. The program supports students pursuing undergraduate degrees in fields related to Information Technology, Engineering, and Business Management. Scholars receive financial assistance for tuition fees, book allowances, and monthly stipends.

Shell Philippines Scholarship Program

The Shell Philippines Scholarship Program supports outstanding Filipino students who wish to pursue degrees in technical and non-technical disciplines. The scholarship provides financial assistance, mentoring, and internship opportunities. Recipients are selected based on their academic excellence, leadership potential, and community involvement.

Megaworld Foundation Scholarship Program

The Megaworld Foundation Scholarship Program aims to support financially challenged but academically gifted students in their pursuit of higher education.

The scholarship covers tuition fees, monthly stipends, and other educational expenses. Scholars are selected based on their academic performance, leadership potential, and socio-economic background.

Are you interested to learn more about scholarship programs? Check out our Scholarship Series.

Education is a fundamental right of every individual, and the government of the Philippines has taken significant steps to ensure that higher education is accessible to all deserving students. One of the most prominent ways in which the government supports students is through various scholarship programs.

These government scholarships provide financial assistance and opportunities for Filipino students to pursue their dreams of higher education and achieve their academic goals.

In this article, we will explore some of the government scholarships available in the Philippines and shed light on the benefits they offer to students.

Government Scholarships in the Philippines

CHED Scholarship Program

The Commission on Higher Education (CHED) offers several scholarship programs to help financially challenged students pursue their college education. One of the notable scholarships under CHED is the Student Financial Assistance Programs (StuFAPs).

StuFAPs include different types of scholarships such as the Full Merit Scholarship, Half Merit Scholarship, and Tulong Dunong Scholarship. These scholarships are awarded to students based on academic performance and financial need, covering tuition fees, stipends, and other related expenses.

DOST Scholarship Program

The Department of Science and Technology (DOST) Scholarship Program is designed for students who wish to pursue a degree in science, mathematics, engineering, or technology-related fields.

The DOST scholarship offers financial support, monthly stipends, book allowances, and even an opportunity for international exposure through their Merit and S&T Undergraduate Scholarships.

PESFA Scholarship

The Private Education Student Financial Assistance (PESFA) program is a scholarship offered by the government through the Technical Education and Skills Development Authority (TESDA). It provides financial assistance to economically disadvantaged but deserving students who want to pursue technical-vocational education and training (TVET) programs in private institutions. The scholarship covers the full cost of tuition fees and other related expenses.

OWWA Scholarship

The Overseas Workers Welfare Administration (OWWA) Scholarship Program aims to provide educational assistance to qualified dependents of Overseas Filipino Workers (OFWs). The program offers scholarships to eligible high school graduates who wish to pursue a college degree.

OWWA scholars receive financial support for tuition fees, book allowances, monthly stipends, and even an opportunity for a one-time educational assistance grant.

AFP Educational Benefit System for Dependents (AFPEBS)

The Armed Forces of the Philippines (AFP) extends educational assistance to dependents of military personnel through the AFPEBS.

This program offers financial support, including tuition fees, stipends, and book allowances, to qualified students enrolled in various degree programs.

GSIS Scholarship Program

The Government Service Insurance System (GSIS) offers scholarships to active members’ children who are pursuing a four- or five-year course in any Philippine university or college.

The scholarship program covers tuition and miscellaneous fees, as well as a monthly stipend.

PNP Educational Assistance Program

The Philippine National Police (PNP) provides educational assistance to qualified dependents of PNP personnel through their scholarship program.

The program covers tuition fees, allowances, and other educational expenses for students pursuing a college education.

Department of Agriculture (DA) Agricultural Scholarship Program

The DA Agricultural Scholarship Program promotes agriculture as a viable career choice. It offers scholarships to students who are interested in pursuing agricultural-related courses.

The program covers tuition fees, book allowances, and stipends.

Department of Health (DOH) Scholarship Program

The DOH offers scholarships for students pursuing health-related courses, such as medicine, nursing, and public health.

These scholarships aim to address the shortage of healthcare professionals in the country and provide financial assistance to students who are passionate about serving in the healthcare sector.

Department of Environment and Natural Resources (DENR) Scholarship Program

The DENR Scholarship Program supports students interested in environmental science, forestry, and other related fields.

It provides financial assistance and opportunities for research and training in environmental conservation and management.

LGU Scholarships

Various local government units (LGUs) in the Philippines also offer scholarships to deserving students in their respective jurisdictions. These scholarships may vary in terms of coverage and requirements, so it’s advisable to check with the LGU’s scholarship office or website for available opportunities.

Are you interested to learn more about scholarship programs? Check out our Scholarship Series.

Education is a powerful tool that can unlock countless opportunities and pave the way for a brighter future. The rising cost of education often poses a significant barrier for many students, especially in developing countries like the Philippines.

A scholarship is more than just a monetary award; it is a life-altering opportunity that empowers students to pursue their dreams, regardless of their financial background. By providing financial assistance, scholarships pave the way for students to attend their dream schools, enabling them to immerse themselves in their chosen field of study and unlock their full potential.

Thankfully, there are numerous scholarship programs available to help aspiring scholars achieve their dreams and build a better future for themselves and their communities. Finding the right scholarship program can be an intimidating task at first, but with the right resources and guidance, it becomes an attainable goal.

Whether you’re a high school graduate, a college student, or even a professional looking to further your studies, this guide will serve as a valuable resource to help you navigate the landscape of scholarship opportunities in the Philippines.

How to Find Scholarship Programs in the Philippines

Research and start by conducting thorough research to identify the available scholarship programs. Several organizations, both public and private, offer scholarships in the Philippines.

Universities, government agencies, NGOs, and private foundations are some of the key providers. Explore their websites, contact information, and eligibility criteria. Consider the specific fields of study and academic levels they support to find programs aligned with your interests and aspirations.

Consult Guidance Counselors and Teachers. Seek guidance from your school’s guidance counselors and teachers who may have valuable insights and information about scholarship opportunities. They can provide you with advice on which programs to target based on your academic performance, extracurricular activities, and personal circumstances.

Utilize Online Databases. There are numerous online databases that compile information about scholarship programs in the Philippines. Websites such as the

Commission on Higher Education (CHED)

Department of Science and Technology (DOST)

Philippine-American Educational Foundation (PAEF)

Attend Scholarship Fairs and Workshops: Stay updated with scholarship fairs and workshops happening in your area. These events bring together scholarship providers, experts, and students interested in pursuing further education.

Network and Seek Recommendations: Connect with individuals who have been recipients of scholarships or who are knowledgeable about the scholarship landscape. Their experiences and insights can prove invaluable in understanding the application process, improving your chances of success, and uncovering lesser-known scholarship opportunities.

Are you interested to learn more about scholarship programs? Check out our Scholarship Series.